SMSF (Self Managed Super Fund) property finance provides the ability to borrow to purchase a residential or commercial investment property with a smsf property loan, allowing direct exposure to real property assets.

Assessment policy varies considerably between lenders (loan to value ratios (LVR), SMSF trustee requirements, advice requirements, acceptable securities and postcode requirments) so it’s important you speak to us before you purchase a property so we can provide the knowledge you need.

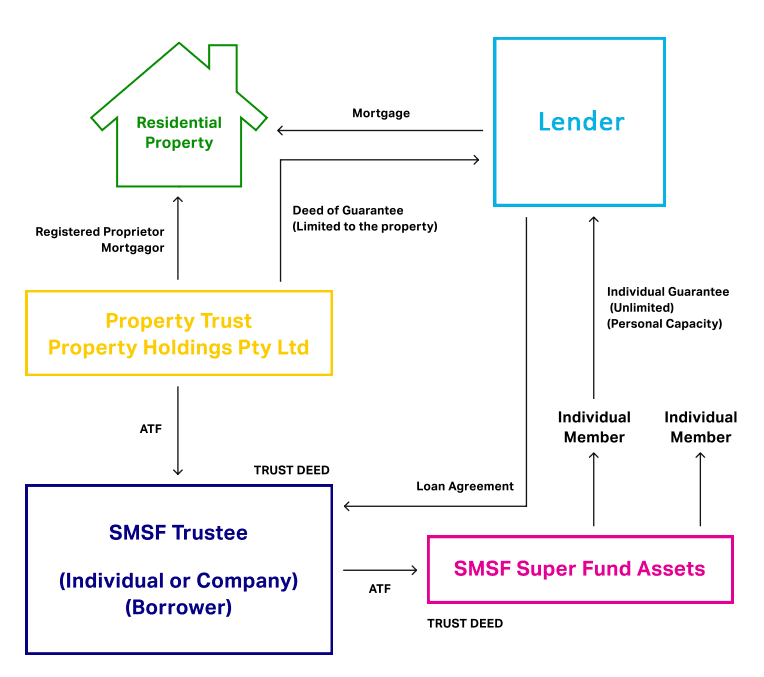

A key reason people elect to manage their own superannuation is the flexibility to choose where their money is invested. Superannuation law allows SMSFs to borrow money to help purchase residential investment property.

SMSF Property Loans can be used to help purchase a single residential or commercial investment property. Funds cannot be used to purchase vacant land, finance construction loans or owner-occupied residential property. All transactions must be at arm’s length and conducted at market rates.

John and Jane Smith have an SMSF with $200,000 in cash and $50,000 in other assets. They would like to buy an investment property within their SMSF. The property, however, is worth $400,000 which means the SMSF doesn’t have enough money to cover the full cost of the purchase. In this instance, the SMSF Trustees can apply for an SMSF Property Loan.

This is a guide only.

Please note the overall loan set up usually takes 6 – 8 weeks. In extreme cases or where supporting documents such as trust deeds are not available when requested, the process can take longer.

The following list is a guide only.

Documents Required- Prior to Settlement